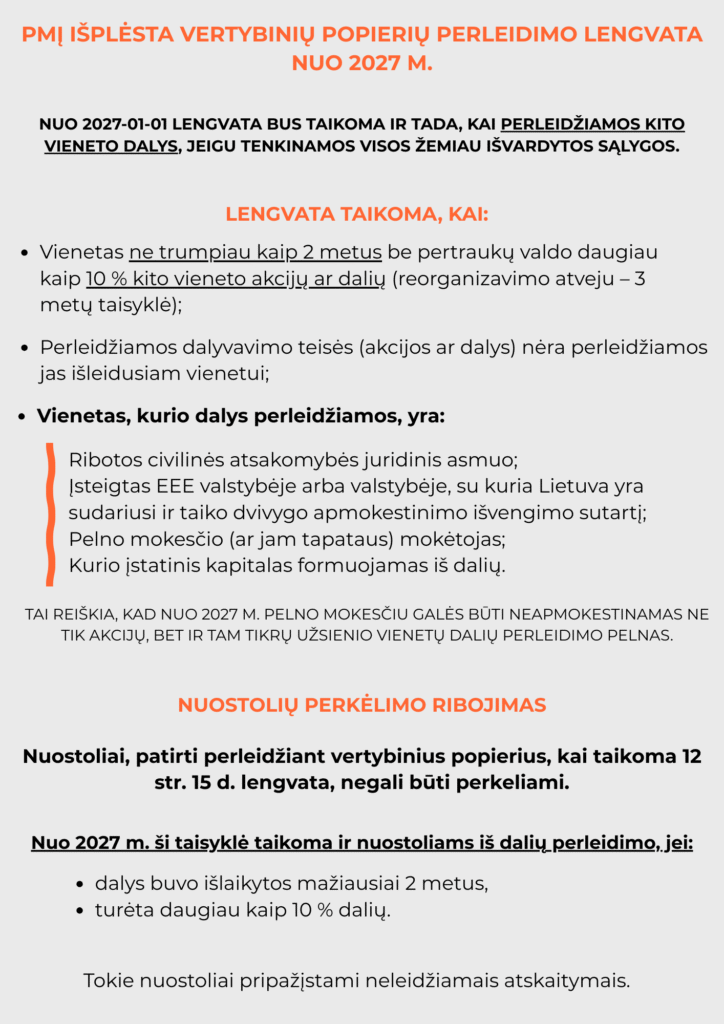

The exemption for transfers of securities is extended in the ITA from 2027.

From 1 January 2027, the relief will also apply to transfers of shares in another unit, provided all the following conditions are met.

The relief applies when:

- An entity owns more than 10% of the shares or interests in another entity for at least 2 continuous years (3-year rule in the case of reorganisations);

- Transferable participation rights (shares or units) are not transferable to the issuing entity;

- The unit whose parts are transferred is:

- A legal person with limited civil liability;

- Established in an EEA State or in a State with which Lithuania has concluded and applies a double taxation agreement;

- Subject to corporation tax (or equivalent);

- The authorised capital of which is made up of parts.

This means that from 2027 onwards, not only gains on the disposal of shares but also gains on the disposal of certain foreign shareholdings will be exempt from corporation tax.

Limitation on loss carry-forward

Losses incurred on the disposal of securities where the benefit of Article 12(15) applies cannot be carried forward.

From 2027, this rule also applies to losses from the disposal of parts if:

- parts have been retained for at least 2 years,

- more than 10 % of the shares held.

Such losses are recognised as non-allowable deductions.