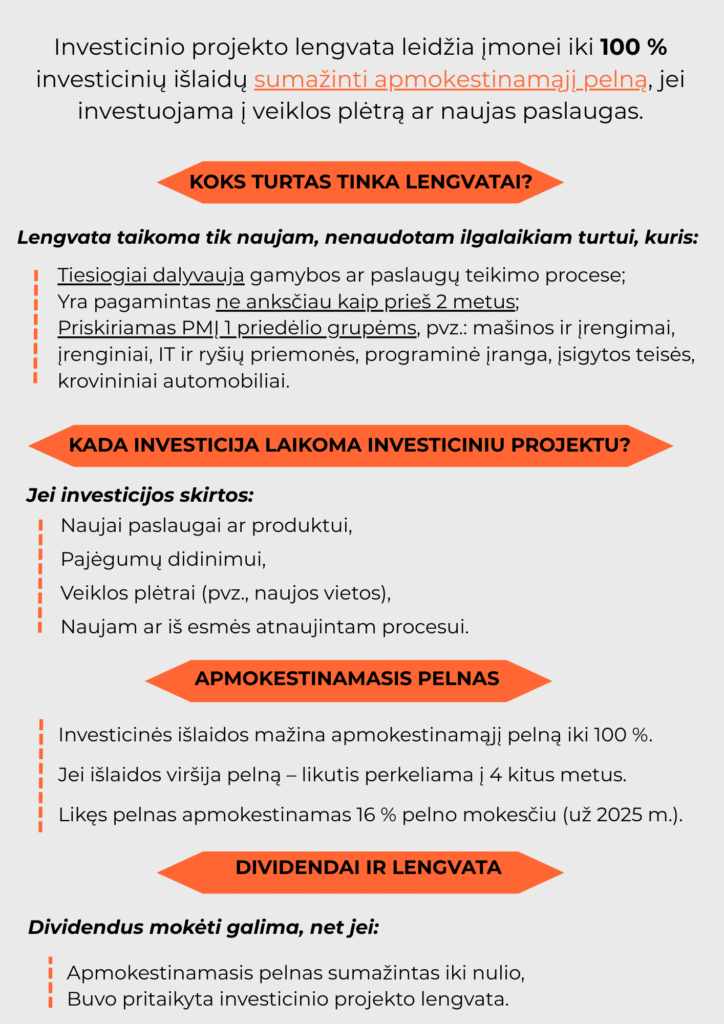

The investment project allowance allows a company to reduce its taxable profits by up to 100% of the investment costs if the investment is in the expansion of its activities or new services.

What assets qualify for the benefit?

The relief applies only to new, unused fixed assets that:

- Directly involved in the production or service delivery process;

- Produced no earlier than 2 years ago;

- Included in the groups in Appendix 1 to the ITA, e.g. machinery and equipment, plant, IT and communication equipment, software, acquired rights, trucks.

When is an investment considered an investment project?

If the investment is for:

- For a new service or product,

- For capacity building,

- For business expansion (e.g. new sites),

- For a new or substantially renewed process.

Taxable profit

- Capital expenditure reduces taxable profits by up to 100%.

- If costs exceed profits, the balance is carried forward to 4 other years.

- The remaining profits are subject to 16% corporation tax (for 2025).

Dividends and relief

Dividends can be paid even if:

- Taxable profit is reduced to zero,

- The investment project allowance was applied.